The Employees’ State Insurance (ESI) scheme plays an important role in providing social security benefits to employees, including medical care, maternity benefits, sickness benefits, and financial support during disability or employment injury. Traditionally, many employers assumed that employees earning more than ₹21,000 per month automatically fell outside ESIC coverage. However, changes introduced under the Code on Social Security, 2020 have altered how wages are calculated for ESI eligibility.

The revised definition of wages means that some employees earning above ₹21,000 may still become eligible for ESIC depending on their salary structure. Employers, HR professionals, and payroll teams must understand these changes to avoid compliance risks and incorrect contribution calculations.

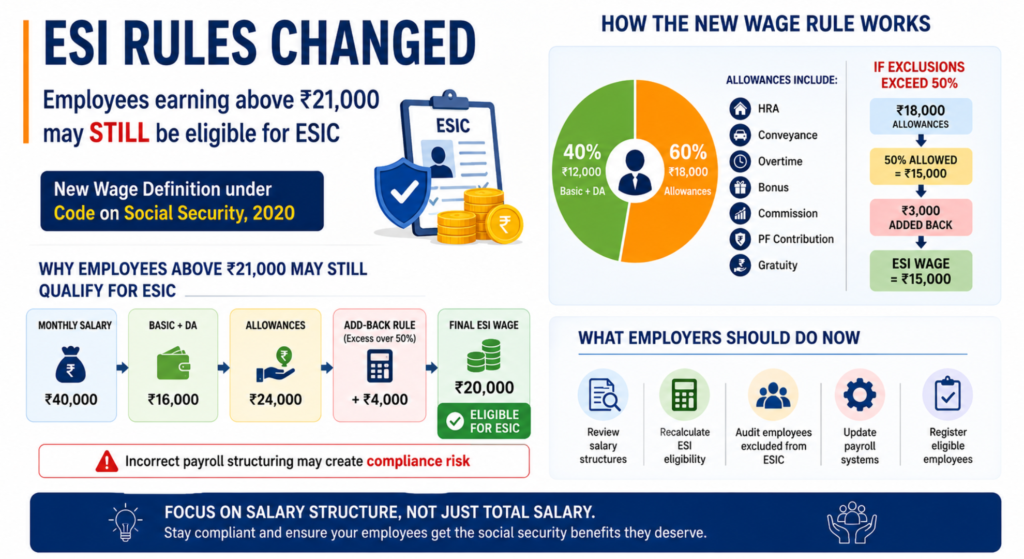

Understanding the New Definition of Wages

Under the revised wage definition, the following salary components are included in wages:

- Basic Pay

- Dearness Allowance (DA)

- Retaining Allowance (if applicable)

Certain salary components continue to remain excluded, such as:

- House Rent Allowance (HRA)

- Conveyance Allowance

- Overtime Allowance

- Bonus

- Commission

- Employer contribution towards PF or pension

- Gratuity

- Other specific allowances and reimbursements

However, the major change lies in the 50% rule.

What is the 50% Rule in ESI Wage Calculation?

The updated regulations state that excluded components cannot exceed 50% of an employee’s total remuneration. If excluded allowances cross this limit, the excess amount must be added back to wages for ESI calculations.

This means salary structuring with high allowances can increase ESI wages even when total monthly earnings appear higher.

For example:

Monthly Salary: ₹30,000

- Basic + DA = ₹12,000

- Allowances = ₹18,000

- 50% of total remuneration = ₹15,000

Since allowances exceed the permitted 50% threshold by ₹3,000, that excess amount gets added back.

Therefore:

ESI Wage = ₹12,000 + ₹3,000 = ₹15,000

The employee may still fall within ESI applicability depending on final calculated wages.

Why Employees Earning Above ₹21,000 May Still Qualify for ESIC

One of the biggest misconceptions among employers is:

Salary above ₹21,000 = No ESIC

This assumption may no longer always be correct.

Consider another example:

Monthly Salary: ₹40,000

- Basic + DA = ₹16,000

- Allowances = ₹24,000

- Allowed exclusion limit (50%) = ₹20,000

- Excess allowances = ₹4,000

The excess ₹4,000 gets added back:

Final ESI Wage = ₹20,000

Since calculated ESI wages remain below the ₹21,000 eligibility threshold, the employee may still qualify for ESIC contributions despite having a higher overall salary package.

This highlights why employers should focus on salary structure rather than only total monthly remuneration.

Impact on Employers and Payroll Teams

The revised wage definition increases the importance of payroll compliance. Incorrect salary structuring or outdated calculations may lead to:

- Wrong ESI deductions

- Non-compliance risks

- Delayed contributions

- Potential penalties during inspections

- Incorrect employee coverage under ESIC

Many organizations may need to reassess employees previously excluded from ESI eligibility.

Payroll systems and salary structures designed under older interpretations may no longer provide accurate calculations.

What Employers Should Do Now

To remain compliant with evolving ESI regulations, employers should take proactive steps:

1. Review Salary Structures

Analyze existing compensation structures and identify employees with high allowance components.

2. Recalculate ESI Eligibility

Evaluate employee eligibility using the revised wage definition instead of relying solely on gross salary.

3. Audit Existing Payroll Processes

Ensure payroll software and internal calculations align with current ESI provisions.

4. Check Previously Excluded Employees

Employees earlier considered outside ESIC coverage may now qualify under the revised calculations.

5. Strengthen Compliance Monitoring

Regular audits can help prevent contribution errors and future liabilities.

Final Thoughts

The new ESI wage definition under the Code on Social Security, 2020 is reshaping how employee eligibility is determined. The introduction of the 50% rule means employers can no longer assume that employees earning above ₹21,000 automatically fall outside ESIC coverage.

Understanding wage composition, recalculating eligibility, and updating payroll practices have become essential for maintaining compliance. Employers who adapt early can reduce risks while ensuring employees receive the social security benefits they are entitled to.